Iron ore faces ‘riot point’ in 2025 as Rio Tinto floods the market Alex GluyasMarkets reporter

Dec 26, 2024 – 11.34am

Iron ore is tipped to trade below $US100 a tonne for most of next year as new supply from Rio Tinto’s long-awaited African project adds to giant stockpiles at Chinese ports, and US tariffs whack steel demand in the world’s second-largest economy.

While markets are divided about the size and effectiveness of stimulus from China – the world’s largest buyer of iron ore – pundits broadly agree that Beijing will roll out further fiscal support in 2025 that should cushion the price of the steel-making ingredient from even heavier falls.

Iron ore’s bearish outlook follows a turbulent year for Australia’s key export, which started 2024 above $US140 a tonne before dropping to $US89 a tonne in September and then recovering to $US110 in early October as Chinese stimulus hopes hit fever pitch.

With the spot price trading at around $US104 a tonne at the year’s end, iron ore has shed more than a quarter of its value this year making it one of the worst-performing major raw materials.

Still, it’s proved more resilient than expected in December after China’s top leaders pivoted on monetary policy for the first time since 2011. This was despite November activity data painting a more sober picture after reporting weaker-than-expected retail sales, fixed asset investment and credit data.

Goldman Sachs expects that China’s economic growth will come close to Beijing’s 5 per cent target for the full year, but noted much of that strength will come from a front-loading of manufacturing and exports ahead of potential US tariffs.

So while physical iron ore markets have tightened heading into the new year, the broker expects that to be temporary, given fundamentals still point to an oversupply. It has forecasted the iron ore price to fall to annual averages of $US95 a tonne in 2025 and $US90 in 2026.

“US tariffs on China, changing nature of Chinese stimulus and new low-cost supply [will] push the market into further surplus and weigh on prices,” said Goldman Sachs commodities strategist Aurelia Waltham. Mounting stockpiles

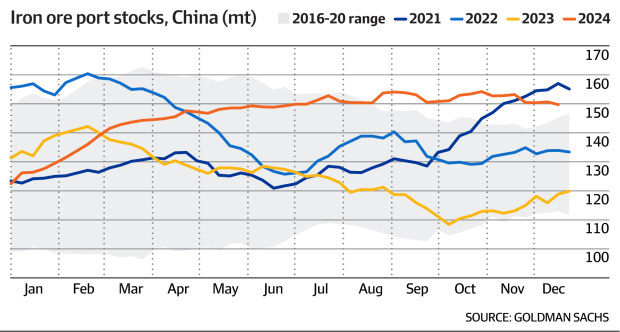

Indeed, China imported 101.86 million tonnes of iron ore in November, meaning the total for the first 11 months of 2024 was almost 9 per cent higher than the five-year average for that period. This contrasts with China’s steel output, which was down almost 2 per cent this year.

This means that China’s steel output is continuing to contract despite iron ore imports rising to near-record levels, exacerbating the mountain of inventory piling up at Chinese ports.

“This all reaches a potential riot point in 2025 when the first iron ore from [Rio Tinto’s] massive Simandou project comes onstream and starts ramping up to full capacity by 2028, flooding the global market,” said Westpac’s head of commodity strategy, Robert Rennie.

Rio Tinto’s long-awaited $34 billion African iron ore project – the largest to be commissioned since Vale’s S11D in 2016 – is scheduled to start production late next year and steadily expand the surplus plaguing physical markets.

Westpac believes prices will be capped in the range of $US105 a tonne to $US110 a tonne as markets move into 2025, before eventually sliding towards $US90 a tonne and below next year.

Still, Westpac’s bearish outlook is far above the typically conservative Treasury forecasts, which economists and analysts said was too low.

In its Mid-Year Economic and Fiscal Outlook, Treasurer Jim Chalmers maintained the government’s assumptions from the May budget that iron ore would fall to $US60 a tonne by the end of the September quarter in 2025.

That was challenged by the Department of Industry Science and Resources’ quarterly outlook, which predicted that iron ore would average $US80 a tonne in 2025, and then drop to $US76 a tonne in 2026.

The federal government uses the free-on-board price, rather than the more widely cited cost and freight price. A $US60 a tonne FOB price is equivalent to a $US67 to $US71 a tonne CFR price.

AMP is among the most bearish on iron ore next year, predicting prices will drop to $US80 a tonne by the middle of 2025.

“The current iron ore price seems too elevated based on demand and supply fundamentals,” said AMP’s deputy chief economist, Diana Mousina.

Ms Mousina is watching for the size of China’s stimulus in terms of the yuan and percentage of gross domestic product, as well as how much is directed to consumers. This would provide an offset from the negative impacts of higher tariffs.

Others are more optimistic about Beijing’s plans to unleash further stimulus next year, with KPMG predicting it will lift iron ore to $US125 a tonne by mid-next year.

“There has been the recognition that broader-based support across traditional sectors, like the real estate and infrastructure development, are necessary in order to underpin economic growth in China,” said KPMG’s chief economist for Australia, Brendan Rynne.

Morgan Stanley is also confident that prices will stay above $US100 a tonne next year, pointing to the resilience of iron ore markets since China’s initial stimulus announcements at the end of September.

Port stocks in China have fallen by 3.4 million tonnes over the past month as steel mills re-stock ahead of the Chinese New Year.

That sets the scene for relatively healthy steel output heading into the first quarter of 2025, according to the US broker, which is tipping iron ore will end next year at $US110 a tonne.