Look at our Top 20 export items:

1. Iron Ore [ potential threats ahead from Simandou and lower China demand ]

2. Coal [ growth falling ]

3. Natural Gas [also falling]

4. Education related [ we're capping international students ! ]

5. Gold

6. Crude minerals

7. Personal travel

8. Wheat

9. Crude petroleum

10. Beef

11. Aluminium ores

12. Charges for intellectual property

13. Professional services

14. Copper ores & concentrates

15. Meat (excl beef)

16. Oil seeds

17. Technical and business services

18. Aluminium

19. Copper

20. Financial services

...half of the top 20 export items are mineral resources related which hog 4 of our top 5.

...and notice something? There isn't anything that is significantly value added

...we are basically ground digger economy that has not diversified and remain highly concentrated, we rested on our commodity laurels while China provided the sole dominant market to which we have become beholden to.

...there are basically 3 disadvantage we have that does not favour us doing manufacturing here -

a. Our small domestic market

b. Our high cost of operations, rendering us uncompetitive [ high wages, high regulatory and tax regime ]

c. Tyranny of distance to major markets except Asia

We ought to be focusing our $ and efforts on high value added items that require specialised knowledge and on which we could potentially differentiate ourselves from the rest of the world

That could include high end medicine, therapies, food bowl for domestic and Asia, event tourism amongst other possible candidates.

Despite our good relations with US, we have even been able to entire US FDI into Australia to develop new tech industries - what do we have to offer? Our proximity to Asia with a sovereignty that respects IP.

..instead of some serious strategic thinking into how to diversify and re-position our economy going forwards, our politicians are tinkering on the edges, lacking vision for reform, and only know how to spend big on things we can't turn back like AUKUS, NDIS and Nuclear plants (if the Libs win).

If we do not change, changes will eventually define Australia.

The big threat to Australia is if the US makes us choose between them and China, a toss up between national security and economy. We had allowed ourselves to be in this position, when we could and should have stayed neutral. The lucky country has blown the (20-year) boom

The story of Australia over the past two decades is a nation that has become incredibly rich thanks in large part to the China-driven commodities super cycle.

Average net worth per household was $1.46 million in 2023, up from $530,500 in 2004, according to the Australian Bureau of Statistics.

National disposable income per person has jumped more than one-third in real terms.

Elevated commodity prices have delivered an unprecedented revenue windfall of $121 billion to the federal budget over just the past three years, Westpac estimates.

The windfall to governments over two decades would be hundreds of billions of dollars. But Australian governments have blown much of the windfall from the mining boom, which may now be approaching an end as China’s economy slows.

Unfortunately, author Donald Horne’s grim diagnosis in the 1960s in his book The Lucky Country that Australia is “a lucky country run mainly by second-rate people who share its luck” appears to be a modern reality.

The bottom line is that spending is permanently higher, debt has blown out, real wages and productivity growth are weak, and despite the extraordinary quarter-century boom, Australia faces a decade of deficits.

Furthermore, just months out from a federal election neither political party has a substantial plan to deal with this reality, even as leading economists agree that spending cuts or tax rises will eventually be inevitable.

Australian National University economist Ashley Craig says Australia has relied on being the lucky country for too long.

“We’ve become very complacent, with little appetite for real reform,” he says. “I worry we will need a very bad period to shock us into getting our act together.”

China’s gift

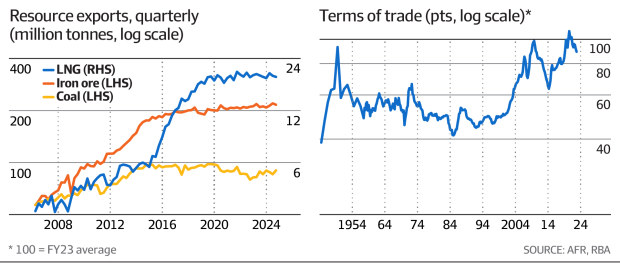

The resources boom began around 2005 as China’s urbanisation led to insatiable demand for commodities including iron ore, coal and gas to power its economy and build homes, factories, office towers, bridges, roads and cars.

Australia’s terms of trade – export prices relative to import prices – soared after China’s massive stimulus in response to the 2008 global financial crisis took a temporary dip from 2012 and surged again from 2016 to extraordinary levels since the pandemic.

The doubling of Australia’s terms of trade delivered the nation a huge pay rise compared to the rest of the world, and was matched only by oil-rich Norway in advanced economies.

Australia recycled the massive increase in national income and government revenues into expanding the public sector, particularly in the past five years. Think the $50 billion National Disability Insurance Scheme, childcare, aged care, health and, more recently, defence.

To be sure, it is a sign of a wealthy and mature economy that governments have spent more on social care. Australians are living longer, and are healthier, wealthier, more educated and travelling overseas more than their predecessors a quarter of a century ago. This is good news.

But the temporary revenue windfall led to a permanent government spending increase of about 2 per cent of GDP compared to pre-pandemic, or more than $50 billion a year.

State government spending and debt have also blown out considerably.

The spending splurge has not been sustainably funded for the long term – either through explicit tax rises, offsetting spending cuts or productivity-boosting reforms to grow the economy faster and lift living standards.

After two budget surpluses, the big hangover was exposed when Treasurer Jim Chalmers handed down the mid-year budget update in December.

Despite near-record government revenue, the budget deficit in underlying terms is forecast to be $26.9 billion (1 per cent of gross domestic product) this year. Cumulative underlying deficits over four years are projected to blow out to $144 billion. But that is not the full story.

The underlying budget balance that treasurers prefer to focus on hides so-called “off-budget” spending, such as taxpayer money for the $30 billion Clean Energy Finance Corporation, the $12 billion Snowy Hydro 2.0 project, the $15 billion National Reconstruction Fund and wiping $16 billion off student debts.

Adding in the government’s extra below-the-line spending, the headline cash deficit is $47.8 billion this year and a whopping $233 billion over four years to 2027-28.

Headline spending of 27.9 per cent of GDP in 2025-26 is projected to be the highest on record, outside of the pandemic. ‘Permanent promises off temporary luck’

Economist Chris Richardson says neither side of politics is tackling the budget problem in the lead-up to the federal election.

“The cost of running Australia has risen,” Richardson says. “That’s been masked by a one-off revenue boom that is just starting to fade.

“I’d prefer to be us rather than, say, the US – whose budget is a mess. Yet, having been handed an enormous windfall, our governments are making the old mistake of permanent promises off the back of temporary luck.”

Huw McKay, a former BHP chief economist and now visiting fellow at ANU, is more glass half full about the past quarter of a century.

McKay, who lived in Singapore for eight years, says there are few countries that have prospered as much as Australia.

“Relative to other countries, there are not too many you’d want to swap with,” he says. “The government balance sheet hasn’t done amazingly well out of the boom, but the household balance sheet has done very well.

“We are substantially wealthier than we were at the opening of the century, and much of it sits in superannuation funds, which is broadly distributed across society.”

Australians have $4.1 trillion locked away in superannuation.

The government’s sovereign wealth fund, the Future Fund, has accumulated $230 billion, from $60.5 billion originally stashed away by Liberals John Howard and Peter Costello in 2006 from budget surpluses and the third phase of the Telstra privatisation.

But the Future Fund today is less than one-tenth of the size of Norway’s sovereign wealth fund, set up to benefit future generations from depleting oil revenue.

Outlook Economics director Peter Downes says Australia could have done better, but it hasn’t been a disaster.

“We haven’t locked much of our boom away in terms of public saving and investment, but we have done so on the private side through the compulsory superannuation system which has built an enormous stock of private wealth,” Downes says.

But Downes says Australia is paying the price for not reforming the tax system in line with former Treasury secretary Ken Henry’s major tax review in 2009 under the Rudd Labor government.

“The demise of the resource rent tax and of the original emissions trading scheme/carbon tax were twin disasters on the tax front which we are still paying for,” he says.

Today, federal gross debt is projected to hit $1.1 trillion in 2026-27. While this is relatively low by international standards at 36 per cent of GDP, it is not representative of a public sector balance sheet that has just experienced a once-in-a-lifetime revenue boom.

Australia’s federal government debt is about one-third of the 100 per cent of GDP in the United States and United Kingdom. Adding in ballooning state government debt, total government debt is about 50 per cent of GDP.

Federal and state spending and debt has ramped up, just as labour productivity growth has slowed sharply.

Strong productivity growth in the 1990s and early 2000s was how Australia delivered faster economic growth and higher real wage increases, and paid for government services through more tax revenue.

Productivity – how efficiently labour produces goods and services – is the key determinant of living standards and contributed more than 80 per cent of income growth for the three decades before the pandemic, the Productivity Commission estimates.

Now, stagnant productivity is contributing to inflation pressures, weaker real incomes and a decline in living standards.

The expansion in the public sector has led to a surge in government-funded jobs.

The jobs boom has helped keep unemployment below 4 per cent. But the flipside is that the surge in government and care economy jobs has contributed to a stagnation in labour productivity.

It is stuck at 2016 levels and has gone backwards 3.9 per cent since mid-2022.

Productivity Commission chairwoman Danielle Wood said in July that it “always has been and always will be difficult” to improve productivity in labour-intensive industries.

“So what that means is as those sectors expand as a share of the economy, as they inevitably will, that will drive down productivity overall, and you have got to work harder elsewhere,” she said. Spending cuts and tax rises needed

Australia faces a nexus of a tight jobs market, stagnant productivity and inflation pressures.

EY chief economist Cherelle Murphy says: “We need a plan to jump-start our productivity through major reforms – including, importantly, to our tax system, trade and education – or we will face higher taxes and cuts to essential services in the future.

“As we approach the election, Australian business needs the political debate to focus on these critical issues.”

Economist Saul Eslake says the government has avoided any substantial decisions on how additional spending should be paid for.

“The government has completely squibbed this task,” he says. “It has been clear for some years now – since before this government came to office in May 2022 – that government spending is permanently on a higher plane.

“That reflects the very clear desire of the Australian public for more spending on health, aged, disability and child care, the consensus across the political aisle that Australia needs to spend more on defence, and the inescapable necessity of spending more on interest as a result of the more than $500 billion increase in federal government net debt since the [2008] global financial crisis.”

Eslake suggests a combination of trimming spending and tax rises will be required. Otherwise, younger workers will face an ever-increasing tax burden.

“It’s going to be paid for by a combination of an ever-increasing personal income tax take on wage and salary earners than those earning income in other ways, and larger budget deficits,” he says.

“In both cases, the burden is falling disproportionately on younger generations.”

Henry warned in a speech in October about the “intergenerational tragedy” younger workers are facing.

“Young workers being denied a reasonable prospect of home ownership; young workers burdened by mountains of public debt, the punishing costs of securing a tertiary education; young workers held back by a tax system that relies increasingly upon fiscal drag.

“Young workers, a declining proportion of the population, are having to pick up the tab.”